In recent years, Malta has witnessed a significant shift in how families approach homeownership and the property market, driven largely by rising property prices and changing economic conditions. One of the most notable trends is the growing practice of gifting property to children, a strategy that underscores the strong role of the family in Maltese society. Today, we explore how a study published by the Foundation for Affordable Housing is analysing this trend that is reshaping homeownership, and its implications for wealth distribution in Malta.

The Family’s Role in Malta’s Housing Market

Like in many Southern European countries, owning a home has always been a priority for the Maltese, with families playing a key role in helping their children achieve this goal. For years, this has contrasted starkly against Northern European nations, where assistance comes from the government by providing housing through renting of social housing. This is reflected in high home ownership rates across the Southern Europeans (76.3%), and even more so amongst Maltese (82%).

Many Maltese families help each other in acquiring property by providing support in various forms. This includes cohabitation (resulting in a high share of adults living with parents), chipping in with financial help, or guaranteeing loans. These are all part of a broader system where parents invest in their children’s future, often with an untold expectation that their children will care for them in their old age.

Rising Property Prices and the Shift to Gifting Property

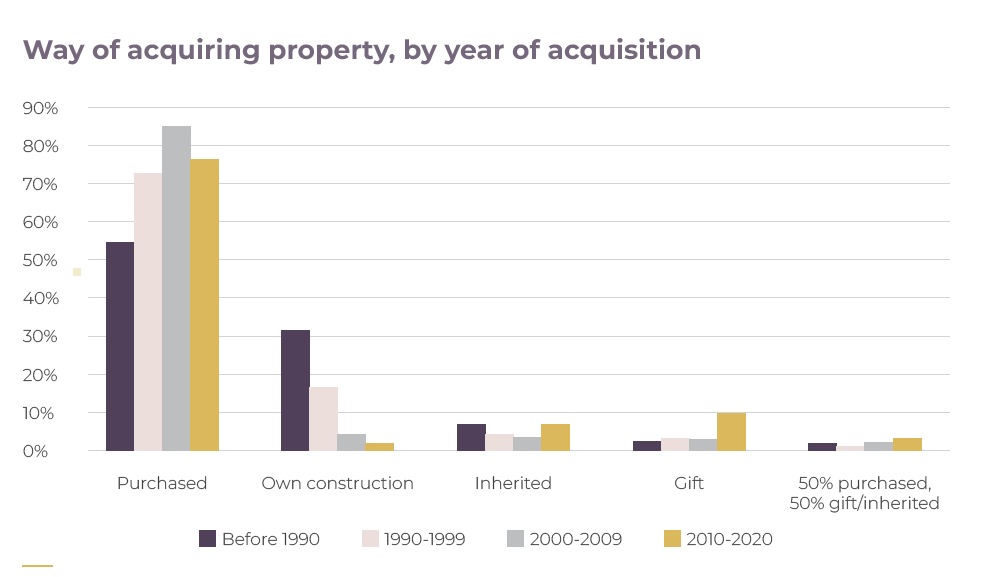

Over the past decade, Malta has experienced strong economic growth, which has attracted migration that in turn led to an increase in property prices. This has inevitably made it harder for first time buyers to purchase their first property. Therefore, to cope with this challenge, more families have been choosing to give property to their children as a gift while they are still alive, rather than waiting to leave it as an inheritance. Dr Dylan Cassar’s recent study, published by the Foundation for Affordable Housing, found that property acquired through gifts or inheritance increased from 10% in the 2000s to 21% in the last decade. By gifting property, parents help their children overcome some of the obstacles in the housing market, providing them with a valuable asset that is likely to appreciate in value over time.

The role of the property market in curbing wealth inequality

These wealth transfers raise important questions about wealth inequality. According to Cassar, homeownership schemes that incentivised families who had received free/subsidised housing in the 1970s and 1980s to pass it on to their children in the form of gifts have ensured that it is not only wealthy families who can transfer property across generations. This differs from other contexts, like the UK, where wealth inequality had a differential impact on the transmission of intergenerational gifts. However, one should remember that this increase in gifting is a strategic response to market pressures.

A recent study by the Central Bank of Malta shows that housing is the most important asset for families across all income levels. Lower-income households rely even more heavily on their homes for wealth when compared to wealthier households. Specifically, 71.2% of the wealth of the poorest half of households comes from their homes. For middle-income families, 69.8% of their wealth is in housing. Even among the wealthiest 10% of households, 50.4% of their wealth is tied up in property. This helps Malta’s inequality figures remain below EU average levels.

In Malta, family support in acquiring property extends beyond gifting homes. Many households, particularly young individuals and couples, increasingly rely on financial assistance from their parents or relatives, often referred to as the “Bank of Mum and Dad”. This support can take various forms, including direct cash transfers, intra-family loans, or loan guarantees.

Comparative studies of European societies show that Southern European countries, including Malta, rely less on cash transfers and more on co-residence. However, when cash transfers are made, they tend to be substantial. The median cash gift was around €29,000. Additionally, about 8% of households received direct financial help when purchasing a home. Informal discussions with banking professionals suggest that this figure may be closer to 30%-40%, particularly as property prices continue to rise. In some cases, families also provide loan guarantees, using their own property or assets as collateral to secure loans for their children.

The future of housing policy

Looking forward, policymakers and society must take these trends into consideration when trying to understand the future of homeownership in Malta. The inability of the banking sector to create financial products that help developers build affordable housing projects, combined with the slowdown in the increase of government social housing options that has been coming since the 1990s, have left a gap from the supply side of the property market that has yet to be addressed.

In an interview with MaltaToday earlier this month, the Foundation for Affordable Housing’s CEO suggested that the joint-venture by the government and the church seems to be heading in the direction of providing such solutions. He explained that, by encouraging investment in affordable housing and other social initiatives together with a well crafted planning policy, Malta could diversify its investment landscape while simultaneously addressing housing needs.

Leave a Reply